Read time: 4.5 mins

Read time: 4.5 mins

The Future of Finance: A Look at Innovation in the Financial Services Industry

There is a massive evolution unfolding in the financial services industry, encompassed in a single abbreviated term:

Fintech.

Fintech is a broad term that has become associated with the application of technological innovation in the financial services industry.1 While the march of technology has always had an impact on the financial services – as it has on every industry – fintech is forcing a rapid evolution in the sector, as disruptive innovations like blockchain have forged new paths, changing the future of finance seemingly overnight.

Considering how quickly things are evolving, it’s worth understanding what lays ahead for fintech and the financial industry to better prepare for the future. In particular, two technologies that are grabbing the attention of both the business world and the public at large are artificial intelligence and blockchain.

Artificial Intelligence

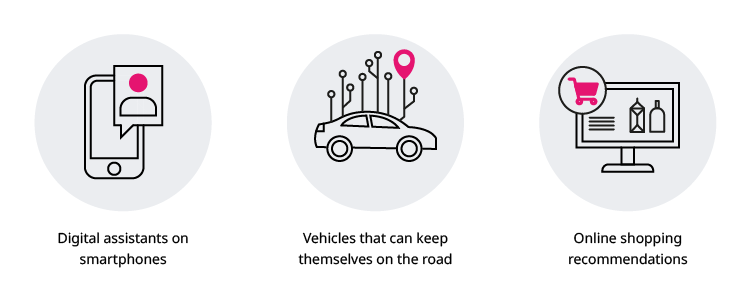

Artificial intelligence (AI) refers to the “ability of a digital computer or computer-controlled robot to perform tasks commonly associated with intelligent beings.”2 AI can already be found in a host of everyday applications:3

In terms of the future of finance and financial innovation, AI is establishing its utility in two key areas: customer service and process automation.

Customer service

One of the most innovative aspects of AI is that its technology and automation abilities enable businesses to learn more about their customers, provide customers with improved support and service, and enhance the customer experience in nearly every way.4

Fintech companies have developed sophisticated methods of interacting with their customers, without the need for direct human intervention: chatbots. Fast becoming the new normal within the financial services industry, chatbots are replacing traditional in-person customer service support. Examples of how this innovation is already improving the financial services industry include faster response times, more personalized customer service, a reduction in customer service costs, and shorter queues, as well as the fact that customers can enjoy these services from the comfort of their own home.5

Process automation

Process automation, which includes robotic process automation (RPA), a popular tool that uses various technologies to automate secretarial tasks, is taking over low-skill manual tasks within the finance industry, while at the same time offering a variety of benefits: Reduced costs, faster processes, reduced manual errors, and greater employee satisfaction.6 One of the most significant benefits of process automation within the financial service industry is that it’s reducing the time and manpower required when performing manual processes. Thanks to the innovative range of AI tech solutions, core financial tasks – such as invoicing, data entry and extraction, and expense management – can now be automated.7

Blockchain

Blockchain, which can be defined as a shared, immutable ledger that securely links blocks of encrypted data transactions in a network, is changing the traditional world of finance.8 For starters, conducting financial transactions is fast becoming a purely online experience. As a result, blockchain has become the medium for recording and storing these kinds of secure financial transactions, including that of cryptocurrencies, or digital tokens, such as Bitcoin and Ethereum.9

This innovative technology means that blockchain also lends itself to several useful applications in the world of finance:

Investing

When it comes to financial transactions, such as investing, blockchain can offer a number of benefits:10

- Improved transparency. Since investment activities are performed on a public ledger, inefficiencies such as fraud can be more easily exposed, leading to reduced risk.

- Added security. Payments and money transfers made via blockchain are faster and more traceable than in traditional banking.

- Lower costs. For investors looking to avoid higher fees, blockchain offers access to financial activities, such as investing, at lower costs usually associated with traditional financial services.

Smart contracts

Simply put, a smart contract is a self-executing contract where the terms of the agreement between two (or more) parties are written into code, operating autonomously on a decentralized blockchain network.11

Unlike traditional, and often more complex, contracts, which typically involve paperwork and third-party validation, smart contracts offer a simpler and more streamlined solution. If the conditions embedded or coded in the program underlying the contract are met, then the action (or actions) described in the contract takes place. If the conditions are not met, then no transaction occurs.12

Moreover, smart contracts come with several useful benefits:13

- Smart contracts are self-executing, which makes them independent and ultimately tamper-resistant.

- They can also guarantee greater security as third parties are not involved.

- They are self-verifying, due to the fact that they automatically source information from external data sources.

- They offer greater transparency thanks to incorruptible codes in the blockchain network.

While these applications offer the potential for greater efficiency in the marketplace, there is still a long way to go before they become truly ubiquitous, and there will be challenges along the way.

The future of financial innovation

Of course predicting the future is no simple task, but the current state of development in the financial services and fintech industries, when looked at carefully, can provide some answers. While the first requirement of any business is to generate revenue, and to increase the amount of revenue being created over time, there are deeper conclusions to be drawn from what technologies these companies are choosing to use, and how they’re using them.

The business applications of AI and its offspring – chatbots and RPA – as well as blockchain, show that organizations are becoming more and more focused on improving the customer experience with technology.14

However, as the financial and fintech industries move forward, there are some challengings facing the rise of technologies like AI and blockchain, which must be tackled for the combined success of the organizations which operate in these spheres:

The need for collaboration

While there is no denying that traditional institutions within the finance industry have been slower to adapt to technological innovation, the disruptive force of fintech companies have compelled banks and other financial organizations to try and keep up with new developments, such as AI and machine learning (ML), and seek out opportunities to collaborate.15

Through collaboration, fintech companies and more established financial institutions will be able to leverage the best of both their offerings. For example, by combining the data and scale of banks with the speed and innovation of fintech, the resulting collaborative financial ecosystem will ultimately benefit both the organizations and their customers.16

Navigating legislation

As exciting as all these future trends and financial service innovations may be, they do bring with them a number of risks and challenges.17 Concerns about data protection, privacy, cybersecurity, data management, and even ownership simply cannot be ignored. But luckily the same technologies that are driving financial services innovation, are also offering solutions for companies trying to keep up to date – which is what makes regulation technology (RegTech) and Supervisory technology (SupTech) so important.18

RegTech is a tech solution designed to help financial institutions manage regulatory compliance, whereas SupTech is responsible for managing risk in the financial system and enforcing regulations. Both these technologies are used to improve efficiency through automation, streamline processes and, more importantly, ensure a degree of oversight when it comes to mitigating risks and ensuring customer protection.19

When taking into consideration the rise of innovative technologies such as AI and blockchain, as well as their potential to help organizations improve their offerings and profitability, including offering a far superior customer experience, it seems clear that the future of finance looks promising.

Are you prepared for a changing financial services industry?

- 1 (Nd). ‘Fintech’. Retrieved from Merriam-Webster. Accessed March 11, 2022.

- 2 Copeland, B. (Mar, 2022). ‘Artificial intelligence’. Retrieved from Britannica.

- 3 Reeves, S. (Aug, 2020). ‘8 Helpful everyday examples of artificial intelligence’. Retrieved from IoT for all.

- 4 (Jul, 2021). ‘15 Ways to leverage AI in customer service’. Retrieved from Forbes.

- 5 Singh, P. (Feb, 2022). ‘Chatbots for financial services: Benefits, examples, and trends’. Retrieved from REVE Chat.

- 6 Dilmegani, C. (Mar, 2022). ‘Finance automation in 2022: Use cases, technologies & benefits’. Retrieved from AIMultiple.

- 7 Baragwanath, T. (Apr, 2021). ‘Finance automation: Automate these six boring business processes’. Retrieved from Spendesk.

- 8 Wojno, M. (Jan, 2022). ‘The future of money: Where blockchain and cryptocurrency will take us next’. Retrieved from ZDNet.

- 9 Wojno, M. (Jan, 2022). ‘The future of money: Where blockchain and cryptocurrency will take us next’. Retrieved from ZDNet.

- 10 Likos, P. (Sep, 2021). ‘How blockchain can transform the financial services industry’. Retrieved from U.S.News.

- 11 (Feb, 2021). ‘Smart contracts in finance: A guide for financial institutions and fintechs’. Retrieved from Algorand.

- 12 (Feb, 2021). ‘Smart contracts in finance: A guide for financial institutions and fintechs’. Retrieved from Algorand.

- 13 Rupareliya, K. (Jul, 2021). ‘How smart contracts are transforming banks and financial institutions’. Retrieved from BusinessofApps.

- 14 Marr, B. (Jan, 2022). ‘The 5 biggest financial services tech trends in 2022’. Retrieved from Forbes.

- 15 Williams III, A. (Feb, 2022). ‘3 key ways banks will collaborate and digitize in 2022’. Retrieved from Insider.

- 16 Williams III, A. (Feb, 2022). ‘3 key ways banks will collaborate and digitize in 2022’. Retrieved from Insider.

- 17 (Sep, 2021). ‘The promise of supervisory technology (SupTech)’. Retrieved from Prove.

- 18 Berman, M. (Jan, 2021). ‘RegTech vs. SupTech: What you need to know’. Retrieved from NCONTRACTS.

- 19 Berman, M. (Jan, 2021). ‘RegTech vs. SupTech: What you need to know’. Retrieved from NCONTRACTS.